June 27, 2025

.png)

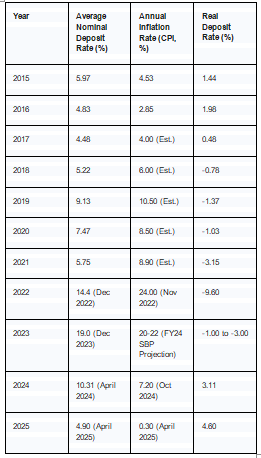

Pakistan's financial landscape (2015-2025) saw high inflation and fluctuating SBP rates, easing to 0.3% in April 2025. Bank deposits consistently yielded negative real returns due to high inflation, with rates recently dropping to 4.90% (April 2025). In contrast, mutual funds, particularly Money Market and Income funds, offered superior real and nominal returns, providing better inflation resilience. Equity funds, though volatile, showed significant appreciation (e.g., 87% in H1 FY2025). Mutual funds generally out performed bank deposits for capital preservation and growth, making them amore attractive investment in Pakistan's dynamic economy.

The SECP-regulated mutual fund sector in Pakistan, which is represented by MUFAP, provides a range of investment choices, such as money market, equities, income, and fixed-return funds. Over the past ten years, the industry has demonstrated a notable increase in Assets Under Management (AUMs)in s of mutual funds increased by 43%. In fiscal year 2021, open-end mutual fund assets climbed 37.2% to PKR 1,018 billion, and by June 30, 2022, they had grown to PKR 1,255.68 billion. The industry's endurance is demonstrated by its steady growth, especially during recessions when investors preferred safer alternatives like money market funds.It points to a maturing financial market where investors are branching out from traditional deposits in order to navigate complicated economic conditions and pursue higher returns, as well as increased investor confidence in professionally managed alternatives.

Pakistan's mutual fund industry offers diverse options, each with distinct risk-reward profiles:

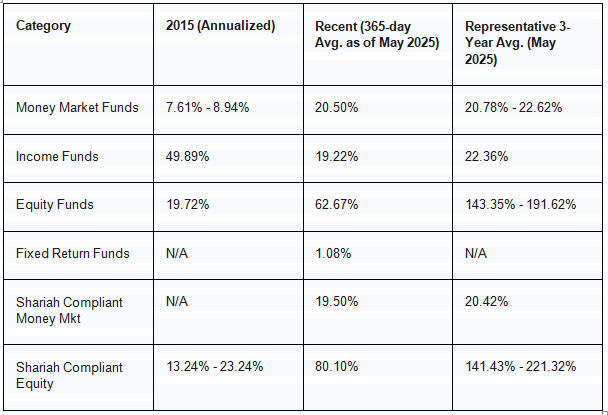

● Money Market Funds: Generally low-risk, these funds focus on short-term liquid assets. They consistently outperformed bank deposits, with many showing 3-year annualized returns in the 20-22% range (e.g., ABL Cash Fund at 22.0375%, NIT Money Market Fund at 22.6193%) in May 2025. Their recent 365-day average return was 20.50%.

● Income Funds: Investing in fixed-income securities for regular income and capital preservation, these funds also delivered strong annualized returns, often close to money market funds. The category saw a 21.81% AUM increase in FY2022. The Alfalah GHP Income Fund had a 3-year annualized return of 22.3573% in May 2025, with a recent 365-day average of19.22%.

● Equity Funds: High-risk, high-reward, these funds invest in stocks. While volatile, they've delivered substantial returns during upturns, with Pakistan's equity market seeing an 87% return in dollar terms in H1FY2025. In May 2025, some equity funds showed remarkable 3-year absolute returns exceeding 140%(e.g., ABL Stock Fund at 143.3507%, AL Habib Stock Fund at 191.6169%). Their recent 365-day average return was 62.67%, with some dedicated funds reaching206.20%.

● Fixed Return Funds: A newer category introduced in H2 FY2022, these are expected to gain interest. While long-term data is limited, some plans like UBL Fixed Return Plan I (U)show very high YTD returns (e.g., 675.31% YTD), though such figures may be outliers or reflect specific product structures.

● Shariah Compliant Funds: These funds have performed comparably or better than conventional funds. As of May 2025, Shariah Compliant Money Market funds had average 365-day returns of19.50%, and Equity funds averaged 80.10%, demonstrating strong performance within their categories.

Note: "N/A" indicates data not explicitly available for the specified period in the provided sources. Recent 365-day average returns are based on overall category averages where available; specific fund returns may vary. Representative 3-Year Averages are based on selected top-performing funds within each category as of May 2025.

It is necessary to take into account both nominal capital preservation and the important component of inflation risk in order to comprehend investment risk in Pakistan.

● Bank Deposits: They have a high risk of inflation even though they appear to be minimal risk for nominal capital. Despite having significant liquidity, this frequently results in negative real returns that reduce purchasing power.

● Money Market and Income Mutual Funds: These provide excellent liquidity and a low-to-moderate risk profile. They are a solid substitute for bank deposits for conservative investors and those with short- to medium-term liquidity requirements because they have continuously produced noticeably higher nominaland real returns.

● Equity Mutual Funds: These investments are high-risk and high-reward. They have the greatest potential for significant wealth growth, while being erratic and dependent on stock market performance.

The conventional wisdom that bank deposits are "safe" is called into question in Pakistan's high inflation climate. Nominal stability is provided, but a loss of purchasing power is inevitable due to their persistently low real yields. On the other hand, because they have traditionally outperformed inflation, slightly riskier assets like money market or income mutual funds are better at preserving real wealth by putting the emphasis on actual purchasing power rather than just nominal increases.

Key Findings and Investment Implications

In Pakistan, the performance of mutual funds and traditional bank accounts has clearly diverged during the last ten years.

● Mutual Funds Consistently Outperform (Nominal): In general, mutual funds—particularly those in the money market and income categories—have provided nominal returns that are noticeably higher than those of typical bank deposits. An 87% dollar-term return for Pakistan's equities market in the first half of FY2025 is an example of how equity funds, despite their greater volatility, demonstrated significant capital gain during favorable market conditions.

● Real Return Challenge for Deposits: One important conclusion is that bank deposits continuously failed to yield positive real returns, especially when inflation was strong, which resulted in a noticeable decline in depositors' purchasing power. For example, the real deposit rate was negative (-5.36%) in April 2025.

● Market Sensitivity of Mutual Funds: The performance of mutual funds, particularly equities funds, is extremely influenced by investor attitude, stock market trends, and macro economic stability. Recoveries spurred a resurgence of interest in stocks, while economic uncertainty caused a shift towards stable assets like money market funds.

● Shifting Investor Preferences: Investor tastes have clearly changed in recent years. A dynamic real location of capital for possibly higher returns is suggested by the renewed interest and rising inflows into equities mutual funds as inflation moderates and fixed-income yields fall as a result of SBP rate cuts.

Active portfolio management is essential for Pakistani investors to combat inflation. Real wealth has not been adequately preserved by traditional bank deposits. For cautious investors and those with immediate requirements, money market and income funds provide a strong edge against inflation by offering superior nominal and real returns with minimal volatility. Despite their inherent volatility, equity funds provide significant capital appreciation potential, making them ideal for investors with longer time horizons and higher risk tolerance. In the end, mutual funds in all categories have typically produced better nominal and real returns than bank deposits, despite the latter's nominal stability. For successful asset preservation and growth, a strategic approach to investing in Pakistan necessitates closely examining mutual fund products, taking into account macro economic factors and individual financial objectives.

2. https://ycharts.com/indicators/pakistan_deposit_interest_rate

3. https://tradingeconomics.com/pakistan/inflation-cpi

4. https://tradingeconomics.com/pakistan/deposit-interest-rate

5. https://www.sbp.org.pk/FSR/2023/Chapter-3.pdf

7. https://ubldigital.com/portals/0/Pdf/Projected-Rates-April-2025.pdf

8. https://profit.pakistantoday.com.pk/2023/12/12/sbp-keeps-policy-rate-unchanged-at-22/

9. https://tradingeconomics.com/pakistan/core-inflation-rate

10. https://www.mufap.com.pk/Upload/WebDoc/Communication/Yearbook2015-Final1403.pdf

11. https://mufap.com.pk/Upload/WebDoc/Communication/Yearbook2016-Final1404.pdf

12. https://www.mufap.com.pk/Industry/IndustryStatDaily?tab=1

13. https://sarmaaya.pk/mutual-funds/mf-categories

14. https://www.mufap.com.pk/Upload/WebDoc/Communication/Year_book_2020-Final1410.pdf

15. https://www.mufap.com.pk/Upload/WebDoc/Communication/Year_Book_2022542.pdf

16. https://www.mufap.com.pk/Upload/WebDoc/Communication/Year_book2018-Final1406.pdf

17. https://beta.mufap.com.pk/Industry/IndustryStatDaily?tab=1

Harvest MFDs is a subsidiary of HG Markets. HG Markets is a TREC holder and broker of both the Pakistan Stock Exchange (MEM 528) and the Pakistan Mercantile Exchange (MEM 293). Licensed and regulated by the Securities and Exchange Commission of Pakistan (SECP), HG Markets holds the Securities Broker Registration Certificate (528/Securities Broker/2024) and the Futures Broker Registration Certificate (BRC 286)